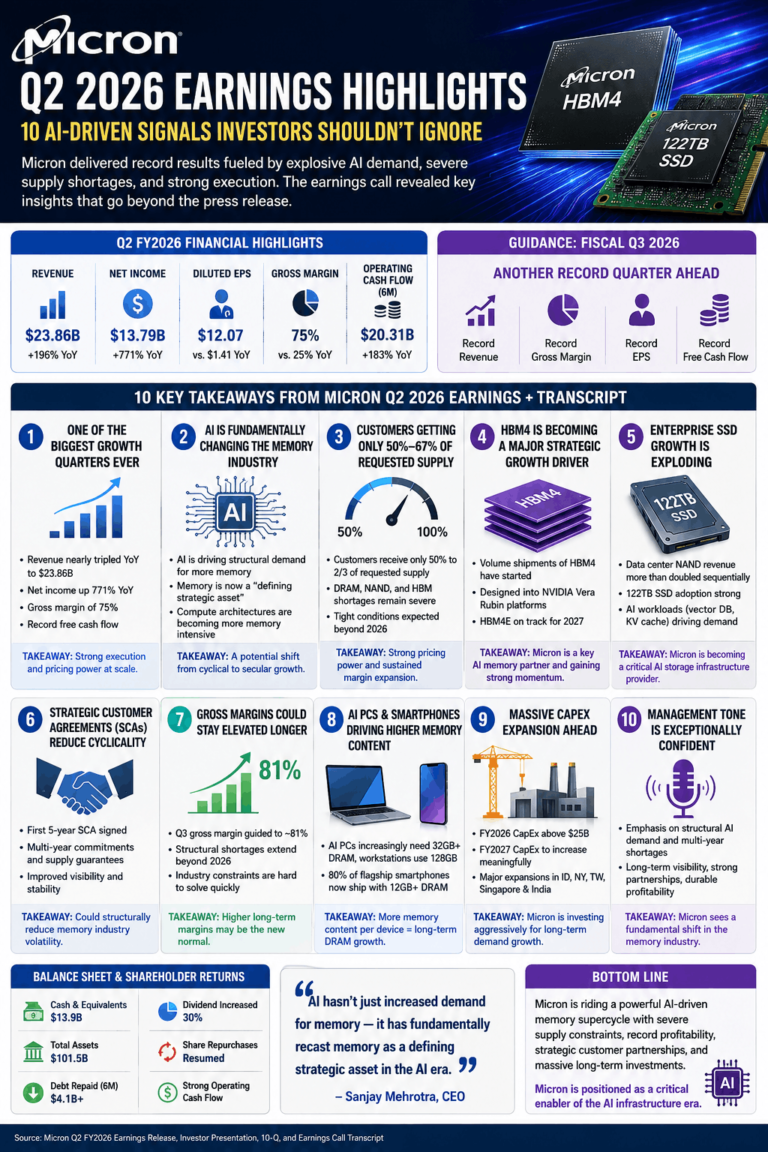

Micron Technology delivered one of the strongest earnings reports in semiconductor history during fiscal Q2 2026, powered by explosive AI demand, severe industry-wide memory shortages, and record profitability.

The company reported massive growth across DRAM, NAND, HBM, enterprise SSDs, and data center products while management repeatedly emphasized that AI is fundamentally reshaping the memory industry.

More importantly, Micron’s earnings transcript revealed several strategic insights that were barely mentioned in the official press release — including extreme supply shortages, structural industry changes, multi-year customer agreements, and expectations for elevated margins beyond 2026.

In this Micron earnings analysis, we break down the most important earnings highlights, guidance, and transcript insights investors should know.