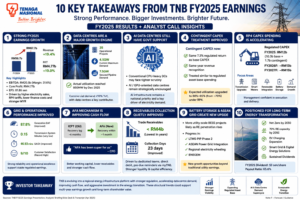

Public Bank Berhad delivered resilient FY2025 earnings despite ongoing net interest margin pressure and a mixed economic environment. The Malaysian banking giant reported record revenue, stable profit growth, improving overseas operations, and strong fee-based income contributions.

For investors looking for Public Bank earnings highlights, earnings analysis, and management guidance, the latest results reveal several important trends that could shape the bank’s growth outlook in 2026.

This earnings analysis explores the 10 biggest takeaways from Public Bank’s latest earnings results, including loan growth, dividend outlook, asset quality, and strategic expansion initiatives.