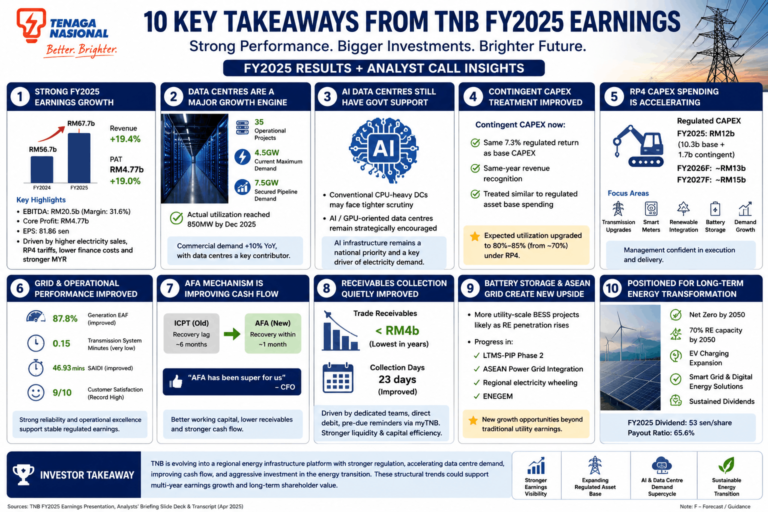

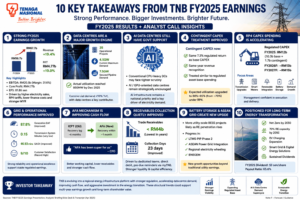

TNB reported FY2025 revenue of RM67.7 billion, up 19.4% year-over-year, while profit after tax climbed 19.0% to RM4.77 billion.

Key financial highlights included:

- EBITDA increased to RM20.5 billion

- EBITDA margin improved to 31.6%

- Core profit rose to RM4.77 billion

- EPS increased to 81.86 sen

The strong performance was driven by:

- higher electricity sales

- implementation of RP4 tariffs

- lower finance costs

- forex gains from stronger MYR against USD and JPY

Importantly, management emphasized that operational improvements — not just forex gains — were the primary earnings driver.

For investors, this signals improving earnings quality and stronger operational execution across TNB’s regulated business.