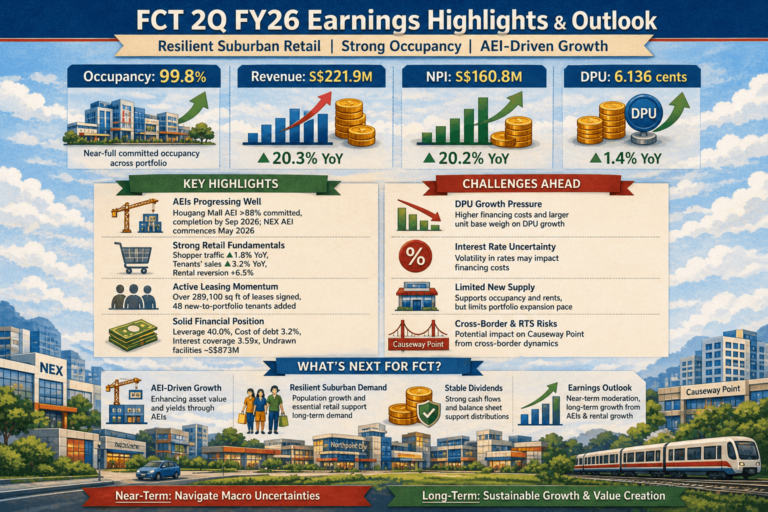

FCT’s 1H FY2026 earnings results demonstrate a high-quality suburban retail REIT with strong fundamentals. Revenue and NPI growth remain robust, supported by near-full occupancy, positive rental reversions, and active leasing momentum.

However, the key challenge remains translating operational strength into meaningful DPU growth. With AEIs progressing and financing costs stabilizing, FCT is well-positioned for steady, albeit moderate, income growth.

For investors, FCT remains a defensive income play with stable yield and visible long-term growth drivers, particularly through its asset enhancement pipeline and resilient suburban retail positioning.