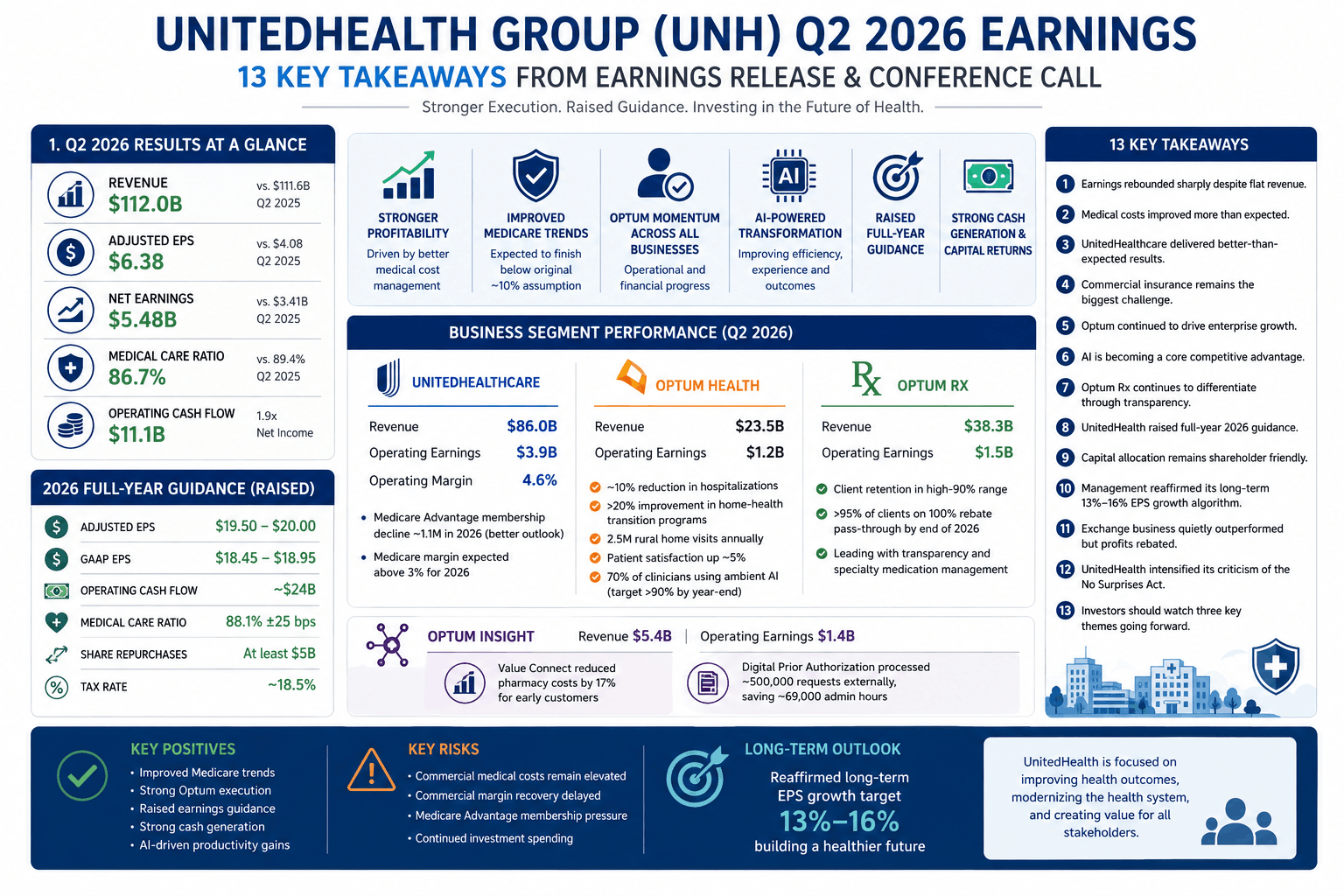

While Medicare improved, executives acknowledged that the commercial business remains under pressure.

Medical cost trends have now risen above 11%, driven by:

- Higher specialty drug costs

- More aggressive provider billing

- Increased coding intensity

- The No Surprises Act Independent Dispute Resolution (IDR) process

As a result, management now expects commercial margin recovery to take longer than previously anticipated, extending beyond 2027.

This was one of the most important new disclosures made during the earnings call and was not included in the earnings release.