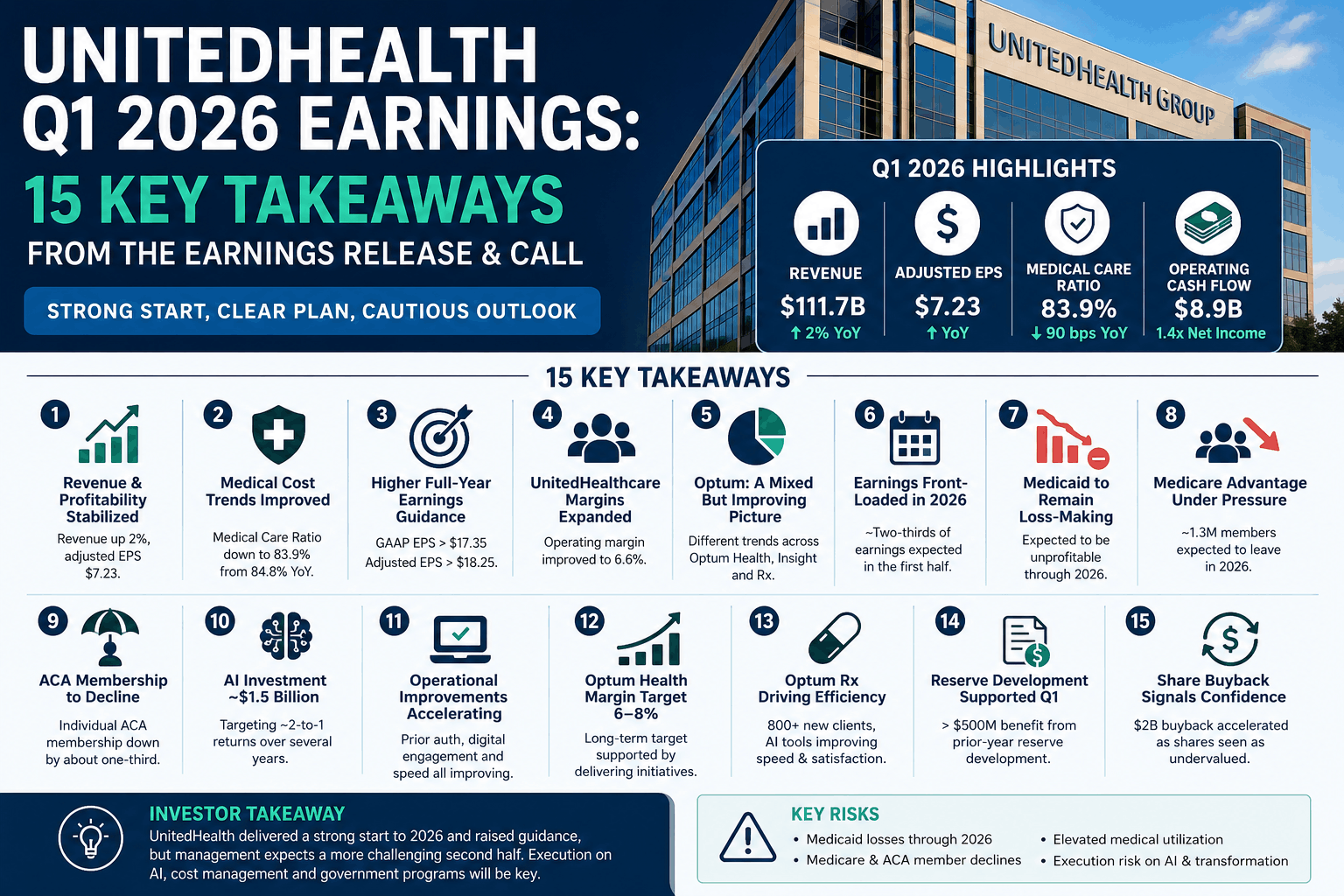

UnitedHealth Group (NYSE: UNH) entered 2026 under intense investor scrutiny after a challenging 2025 marked by elevated medical costs, Medicare Advantage pressure, and organisational restructuring. While the company’s first-quarter earnings showed improving operational performance, the accompanying earnings call painted a much more nuanced picture of the road ahead.

The earnings release highlighted stronger medical cost management, improved cash generation, and raised full-year guidance. However, management used the conference call to explain why investors should avoid extrapolating the strong first quarter, revealing several operational details and strategic initiatives that never appeared in the press release.

Here are the biggest takeaways from both the earnings release and the earnings call.