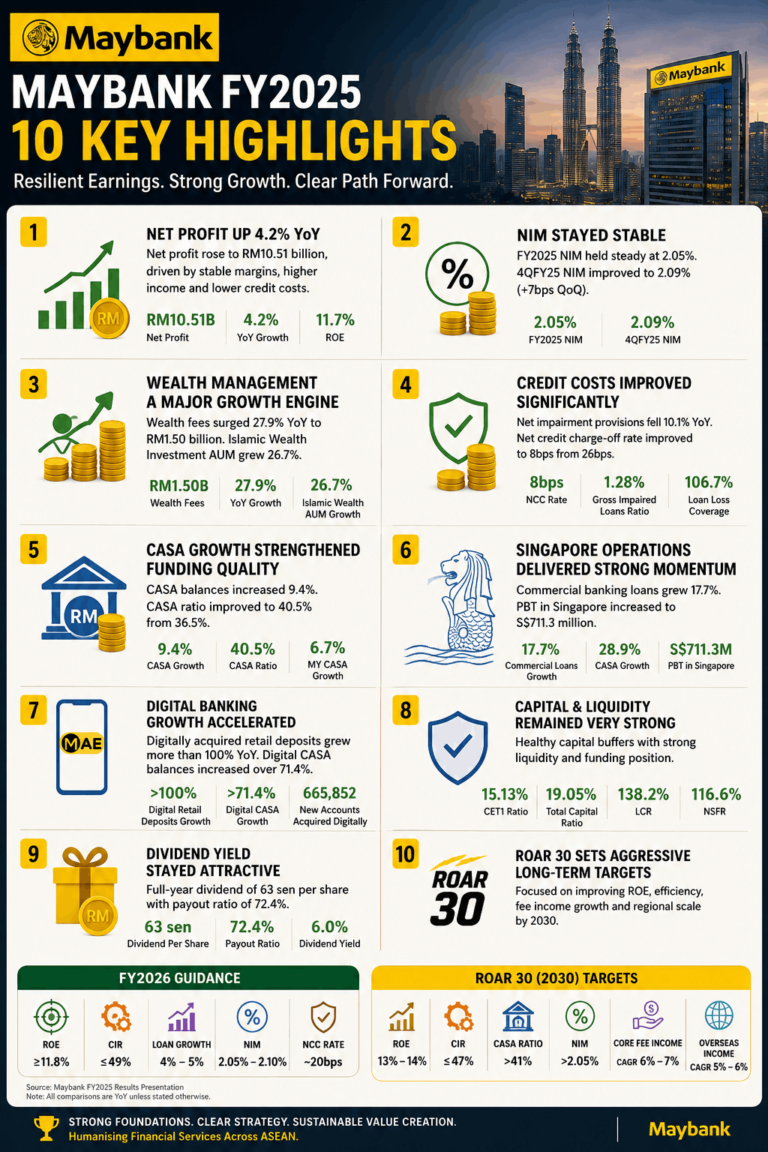

Malayan Banking Berhad delivered resilient FY2025 earnings results despite a challenging regional banking environment marked by lower interest rates, global uncertainty, and slower loan growth across ASEAN. The bank reported stronger profitability, improving asset quality, robust fee income growth, and stable margins while also launching its new long-term strategic roadmap, ROAR 30.

For investors seeking insights into Maybank earnings highlights, earnings analysis, growth outlook, and management guidance, the latest FY2025 results reveal a bank focused on disciplined execution, digital expansion, wealth management growth, and regional scaling opportunities.

Below are the 10 most important takeaways from Maybank’s latest earnings report and investor presentation.