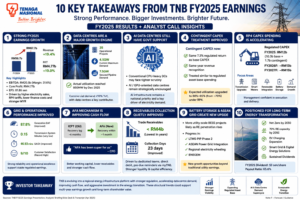

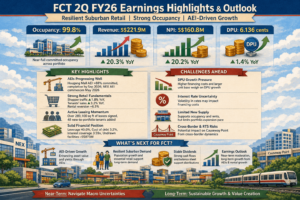

IGB REIT delivered a very strong start to FY2026, with earnings boosted by its latest acquisition and resilient mall performance. Let’s break down the key highlights and what investors should watch next.

Conclusion: Transition Phase, Not Structural Decline

Bull case

Strong earnings momentum

High occupancy, resilient assets

Accretive acquisition already delivering

Watch-outs

Retail sector sensitivity to consumer spending

Rising costs could compress margins

Overall: IGB REIT remains a high-quality retail REIT with visible growth, especially post-Southkey — but future upside will depend on consumer strength and execution

Thank you for reading this post. If you enjoy this post, please share it with your friends or family members. Let’s get life transformed together! Many thanks.