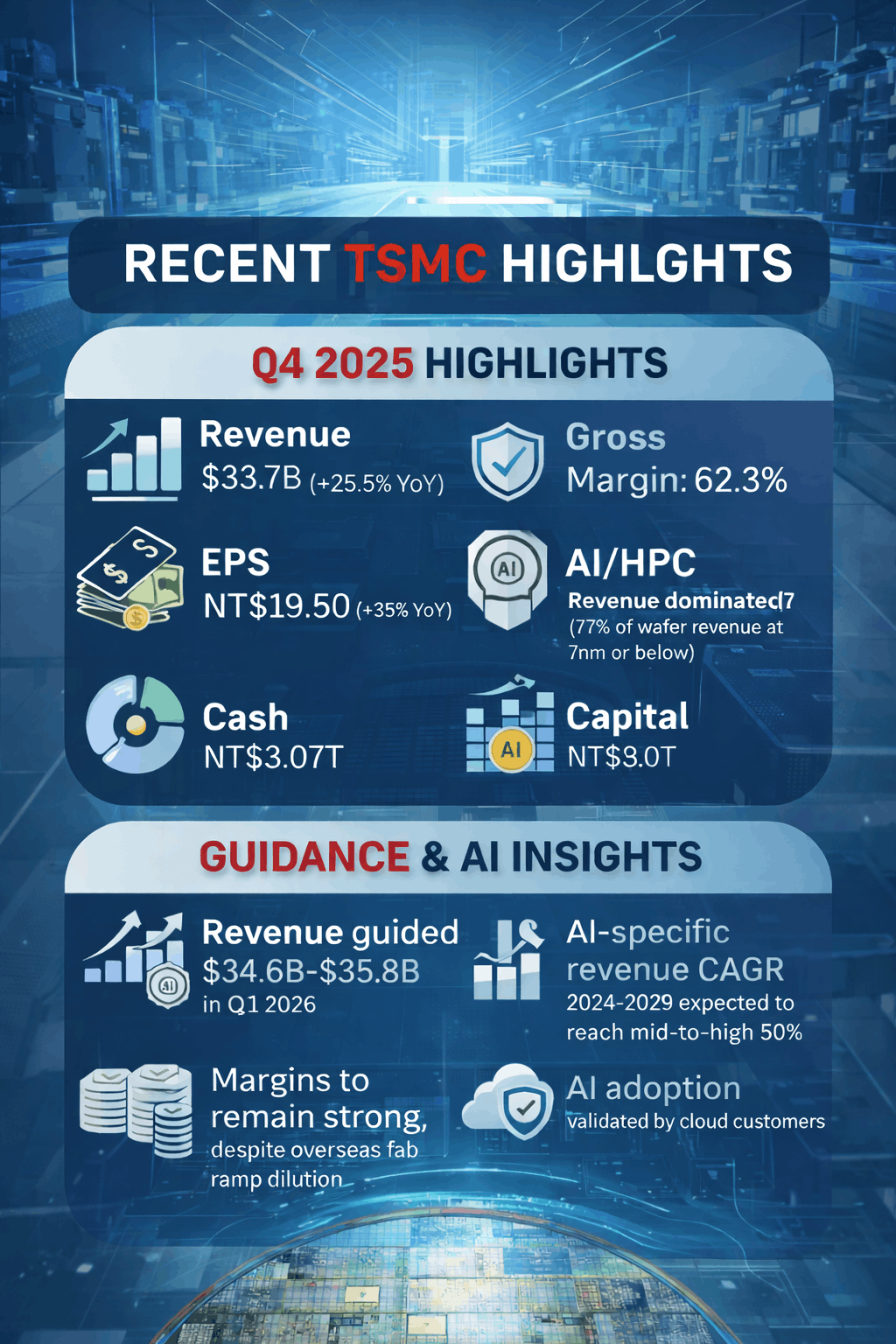

In the fourth quarter of 2025, TSMC reported revenue of US$33.73 billion, exceeding guidance and growing 25.5 percent year over year. In NT dollar terms, revenue reached NT$1.05 trillion, up 20.5 percent year over year. Profitability expanded meaningfully, with gross margin rising to 62.3 percent and operating margin reaching 54.0 percent. Net profit margin climbed to 48.3 percent, reflecting strong utilization and favorable product mix.

Net income attributable to shareholders increased 35 percent year over year to NT$505.7 billion, while diluted earnings per share rose to NT$19.50. These results confirm that TSMC is converting AI-driven demand into real earnings power rather than just top-line growth.

Advanced technologies continued to dominate revenue contribution. In the fourth quarter, 3-nanometer accounted for 28 percent of wafer revenue, 5-nanometer for 35 percent, and 7-nanometer for 14 percent. Overall, 77 percent of wafer revenue came from technologies at 7-nanometer and below, underscoring how central leading-edge nodes have become to TSMC’s business.