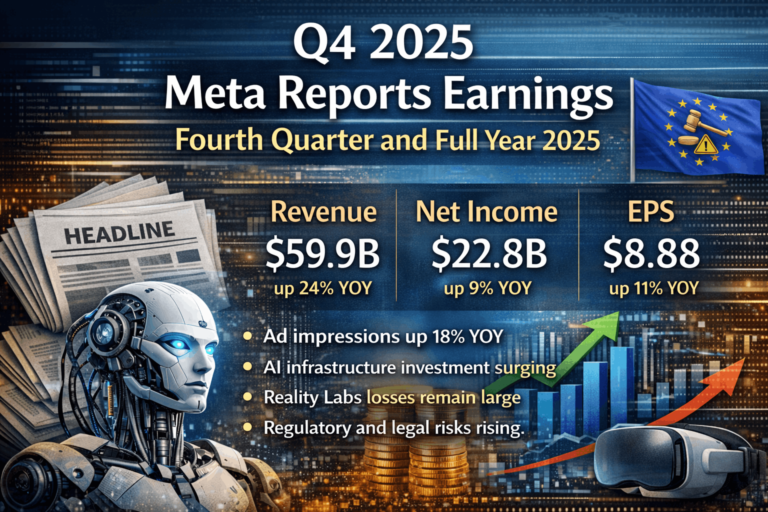

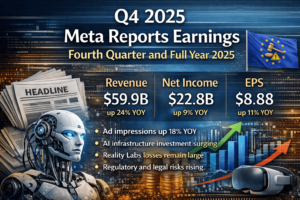

Meta delivered about 59.9B revenue in Q4 2025, up about 24% YoY, and about 201B for full year 2025, up about 22% YoY. For a company already at mega scale, this is extremely strong growth.

Why it matters

This confirms Meta is still gaining share in global digital advertising despite competition from TikTok, retail media networks, and AI search shifts.