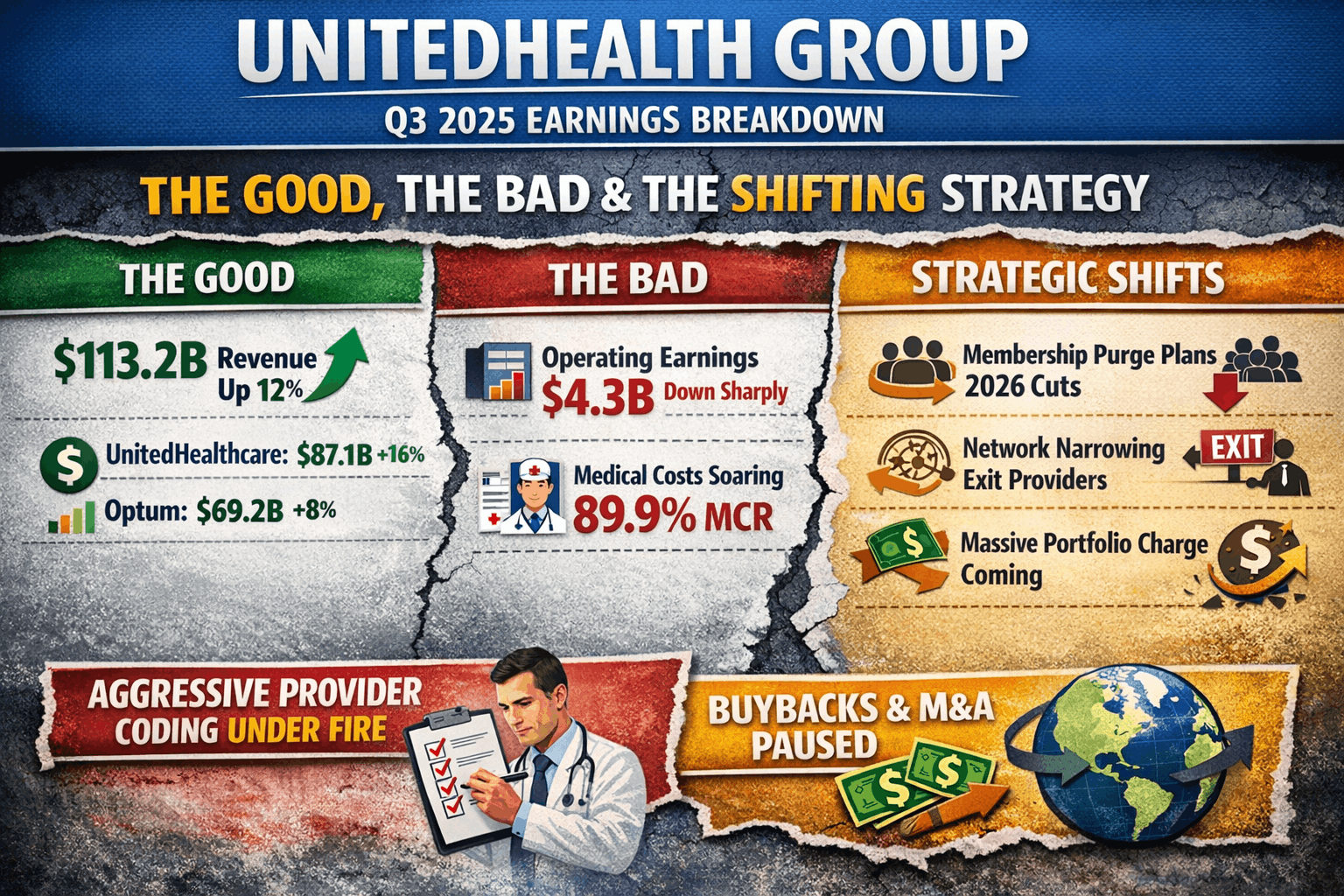

UnitedHealth Group (UNH) released its Q3 2025 earnings this week, and the headline numbers only tell half the story. While revenues are up, the company is quietly preparing for a massive strategic pivot. From “aggressive provider coding” to a planned membership purge, here is the breakdown of the good, the bad, and the strategic shifts revealed in the fine print.