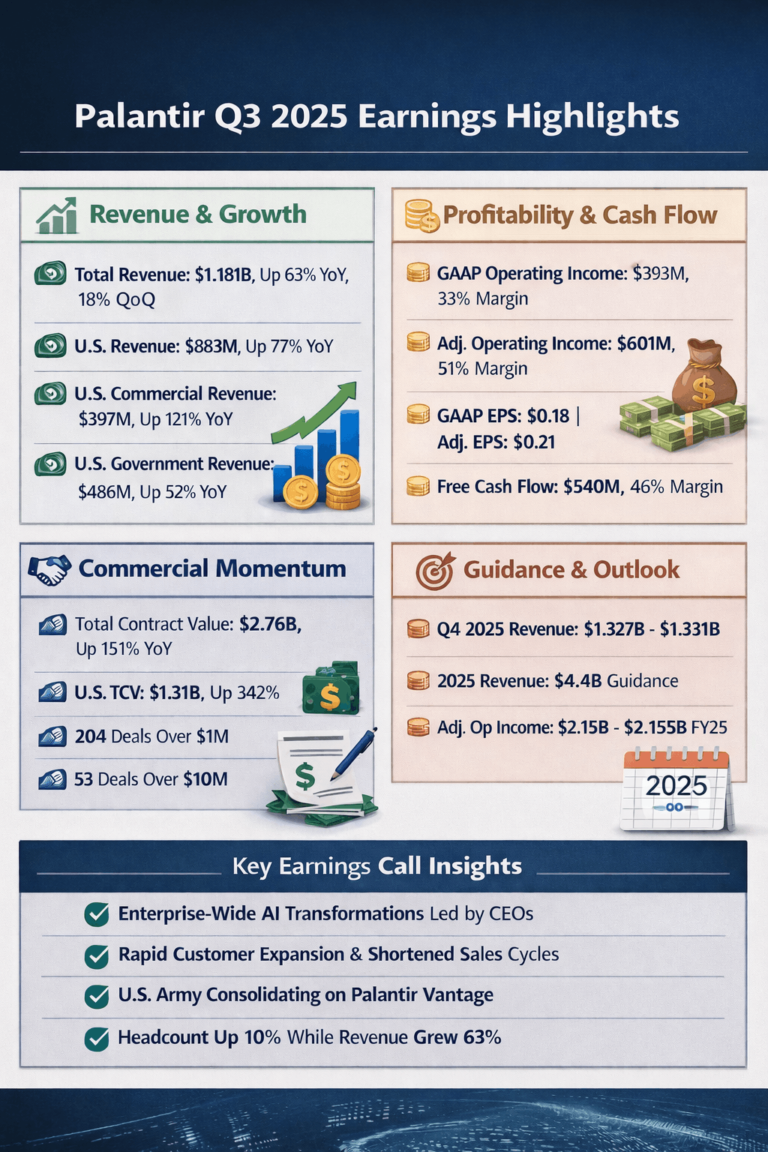

Revenue and growth

Total revenue: $1.181 billion, up 63% year over year and 18% quarter over quarter

US revenue: $883 million, up 77% year over year

US commercial revenue: $397 million, up 121% year over year and 29% quarter over quarter

US government revenue: $486 million, up 52% year over year

Profitability and cash flow

GAAP operating income: $393 million, 33% margin

Adjusted operating income: $601 million, 51% margin

GAAP net income: $476 million, 40% margin

GAAP EPS: $0.18

Adjusted EPS: $0.21

Adjusted free cash flow: $540 million, 46% margin

Cash, cash equivalents, and short-term treasuries: $6.4 billion

Commercial momentum and deals

Total contract value (TCV): $2.76 billion, up 151% year over year

US commercial TCV: $1.31 billion, up 342% year over year

US commercial remaining deal value (RDV): $3.63 billion, up 199% year over year

Deals closed in Q3:

204 deals over $1 million

91 deals over $5 million

53 deals over $10 million

Customer count: up 45% year over year

Rule of 40 and efficiency

Rule of 40 score: 114%

Adjusted operating margin: 51%

Strong operating leverage alongside rapid growth